The Corporate Sustainability Reporting Directive is reshaping how maritime companies disclose environmental data. Here is what falls within scope, what the timeline looks like, and how to prepare.

The Corporate Sustainability Reporting Directive (CSRD) is the EU's most significant expansion of corporate sustainability disclosure requirements to date. It replaces the Non-Financial Reporting Directive (NFRD) and dramatically broadens both the scope of companies required to report and the depth of information they must provide.

For maritime companies, CSRD is not a distant regulatory development — it is an active compliance requirement. Large shipping companies, shipyards, marine equipment manufacturers, and port operators that meet the size thresholds are directly in scope. Smaller companies in the maritime supply chain are indirectly affected, as their customers will need supply chain data to complete their own disclosures.

The directive requires reporting against the European Sustainability Reporting Standards (ESRS), a set of detailed disclosure standards developed by the European Financial Reporting Advisory Group (EFRAG). For climate-related reporting, ESRS E1 is the primary standard, and it requires far more than what most maritime companies have historically disclosed.

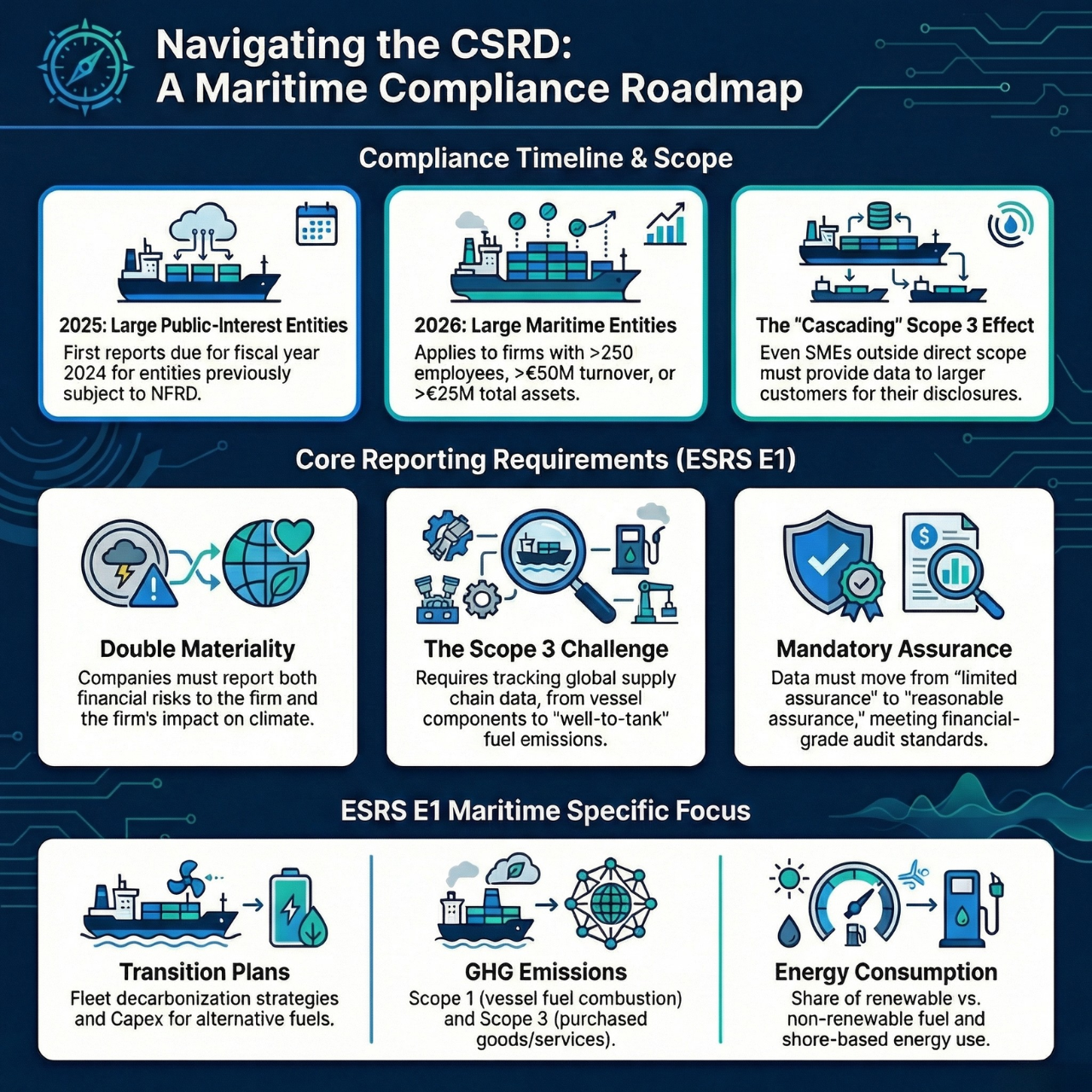

CSRD applies in phases based on company size and listing status. Large public-interest entities (already subject to NFRD) began reporting in 2025 for fiscal year 2024. Other large companies — those meeting at least two of three criteria: more than 250 employees, more than EUR 50 million in net turnover, or more than EUR 25 million in total assets — report from 2026 for fiscal year 2025.

Listed SMEs report from 2027 (with an opt-out until 2028), and non-EU companies with significant EU operations report from 2029. The 2025 Omnibus proposal has introduced potential modifications to simplify requirements for certain companies, but the core framework remains intact for large entities.

In the maritime context, this captures most major shipowners, ship management companies, classification societies, large shipyards, and marine equipment OEMs operating in Europe. Companies headquartered outside the EU but with substantial EU-generated revenue may also fall within scope under the third-country provisions.

Even companies not directly in scope face indirect obligations. When a large shipowner must report Scope 3 emissions, it needs data from its suppliers. This cascading data requirement means that maritime suppliers of all sizes are increasingly being asked for environmental product data, whether they are formally subject to CSRD or not.

ESRS E1 (Climate Change) is the most detailed of the environmental standards and the one most immediately relevant to maritime companies. It requires disclosure across several areas.

Transition plans: companies must describe their plans for climate change mitigation, including targets, actions, and resources allocated. For shipping companies, this means articulating how the fleet will decarbonise, what alternative fuels or technologies are being considered, and what capital expenditure is planned.

GHG emissions: disclosure of Scope 1, Scope 2, and material Scope 3 emissions is required, using the GHG Protocol methodology. For maritime companies, Scope 1 (vessel fuel combustion) is typically the largest category and the most straightforward to measure. Scope 3 — particularly Category 1 (Purchased Goods and Services) and Category 2 (Capital Goods) — is where the data challenge lies.

The standard requires companies to disclose the methodologies used for Scope 3 estimation, including whether spend-based, average-data, or supplier-specific approaches were applied. It also requires explanation of significant estimation uncertainties and the plans for improving data quality over time.

Energy consumption and mix: companies must report total energy consumption, the share from renewable versus non-renewable sources, and energy intensity metrics. For shipping, this includes both vessel fuel consumption and shore-based energy use.

Climate-related risks and opportunities: physical risks (e.g., extreme weather affecting operations, sea-level rise affecting ports) and transition risks (e.g., carbon pricing, fuel availability, regulatory changes) must be assessed and disclosed.

For most maritime companies, Scope 3 reporting is the most demanding element of CSRD compliance. The reasons are structural.

Maritime supply chains are global, fragmented, and often involve multiple tiers of suppliers. A single vessel may contain components from hundreds of suppliers across dozens of countries. Collecting environmental data from this supply base is a logistical challenge that goes beyond what most procurement functions are currently equipped to handle.

The GHG Protocol allows different levels of data quality for Scope 3, and ESRS E1 acknowledges that data quality will improve over time. However, the standard expects companies to demonstrate a credible trajectory — starting with spend-based screening and progressively moving toward activity-based and supplier-specific data for material categories.

For maritime companies, the material Scope 3 categories are typically purchased goods and services (vessel components, marine chemicals, consumables), capital goods (newbuildings, major retrofits), and fuel- and energy-related activities not included in Scope 1 or 2 (well-to-tank emissions).

A distinctive feature of CSRD is the double materiality principle. Companies must assess climate topics from two perspectives: financial materiality (how climate change affects the company's financial position) and impact materiality (how the company's activities affect the climate).

For a shipping company, financial materiality might include the cost impact of EU ETS carbon pricing, the risk of stranded assets if vessels cannot meet future efficiency standards, or the opportunity cost of not transitioning to lower-carbon fuels. Impact materiality covers the company's actual GHG emissions and their contribution to climate change.

Both dimensions must be assessed, and a topic is material if it is significant on either dimension. For most maritime companies, climate change will be material on both counts, making ESRS E1 disclosure mandatory rather than discretionary.

CSRD introduces mandatory assurance of sustainability disclosures. Initially, limited assurance is required — meaning an auditor provides a moderate level of confidence that the disclosures are free from material misstatement. The EU intends to move toward reasonable assurance (the same standard applied to financial statements) over time.

For maritime companies, this means that sustainability data will be subject to audit scrutiny. The methodologies used for emission calculations, the data sources, the assumptions, and the internal controls around data quality will all be examined. Companies accustomed to treating sustainability reporting as a communications exercise will need to adopt the rigour of financial reporting.

Practical implications include maintaining an audit trail from reported figures back to source data, documenting methodological choices and their rationale, implementing internal review processes, and ensuring consistency between sustainability and financial disclosures.

In early 2025, the European Commission proposed modifications to CSRD through the so-called Omnibus package, aimed at reducing the reporting burden, particularly for smaller companies. Key proposed changes include raising the size thresholds (potentially exempting companies with fewer than 1,000 employees in the initial phases), introducing a voluntary simplified standard, and extending certain timelines.

For large maritime companies, the core requirements remain largely unchanged. The Omnibus proposal primarily affects the phasing and scope for smaller entities. However, it has created uncertainty in the market, with some companies using it as a reason to delay preparation. This is risky: the fundamental direction of travel — mandatory, assured, detailed sustainability reporting — is not in question. Companies that delay preparation now will face a compressed timeline when the final rules crystallise.

Preparation for CSRD should proceed in parallel tracks. The first is a double materiality assessment: identifying which ESRS topics are material for the company and therefore require disclosure. For most maritime companies, E1 (Climate Change) will be material, and several other standards (E2 Pollution, E5 Circular Economy, S1 Own Workforce) are likely material as well.

The second track is data infrastructure: establishing the systems and processes needed to collect, validate, and report the required data. For climate data, this means building a GHG inventory covering Scopes 1, 2, and 3, with documented methodology and a clear plan for improving data quality.

The third track is governance: ensuring that sustainability reporting is integrated into the company's governance structure, with clear ownership, board-level oversight, and internal controls comparable to those for financial reporting.

The fourth track is stakeholder engagement: particularly supply chain engagement for Scope 3 data. Building relationships with key suppliers, establishing data collection processes, and communicating expectations early gives the supply chain time to develop the capabilities needed.

CSRD represents a step change in sustainability disclosure for maritime companies. The requirements are detailed, the timeline is near, and the assurance framework means that the data must be credible, not just complete. For companies that have been reporting voluntarily, the transition is manageable. For those starting from a low base, the preparation effort is significant but clearly defined. The practical first step is to complete a double materiality assessment and begin building the Scope 3 data infrastructure — the rest follows from there.